Microsoft has pumped $13 billion into OpenAI and Amazon put $4 billion into Anthropic. Other investments Microsoft and Amazon have made into AI startups also drive sales of compute, storage, and network capacity, enough to move the revenue and profitability of Microsoft Azure and AWS in any quarter. Ditto for Alphabet, which has invested $2.55 billion in Anthropic. It is making the round trip out of the Microsoft, Amazon, and Google investment back doors to OpenAI and Anthropic and then coming back into the same companies through cloud revenue. Until we get clarity on how big the AI partnership investment that is really capacity backlog from such deals, and how much is being burnt off each quarter, we should be careful about cloud revenue growth. How much came from AI startups these companies have stakes in and who got such stakes only because the companies had to spend most of that money on cloud capacity to train their models?

Here’s a question for you: How much of the growth in cloud spending at Microsoft Azure, Amazon Web Services, and Google Cloud in the second quarter came from OpenAI and Anthropic spending money they got as investments out of the treasure chests of Microsoft, Amazon, and Google?

We think this is a very good question, considering that Microsoft has pumped a cumulative $13 billion into OpenAI and Amazon has pumped $4 billion into Anthropic. We do not know what other investments that Microsoft and Amazon have made into AI startups that also turn out to drive sales of compute, storage, and network capacity on their infrastructure, but the amount could be significant. Like enough to move the revenue and profitability of Microsoft Azure and AWS in any given quarter. Ditto for Google parent Alphabet, which has invested $2.55 billion thus far in Anthropic.

All of this money is not spent all at once, of course, but it is making the round trip out of the Microsoft, Amazon, and Google investment back doors to OpenAI and Anthropic and then coming back into the same companies through the cloud revenue front doors. And so, until we get some clarity on how big the AI partnership investment that is really capacity backlog from such deals, and how much is being burnt off each quarter, we should be careful about overreading any statements about cloud revenue growth from Microsoft, AWS, and Google.

We don’t know enough to make a good guess, but heaven knows we are tempted to do so. The deals mentioned above for OpenAI and Anthropic alone come to almost $20 billion together, and we think the vast majority of it is to cover the cost of cloud capacity to train and test generative AI models. There might be another long tail of hundreds of AI startup deals that represent another hunk of money, and it is hard to say how much. GPU capacity is a kind of currency these days – call it FP16coin, we suppose.

Anyway, we will come back to this sugar daddy boomerang effect after we take a look at the revenue streams from the AWS, Microsoft, and Google clouds. Let’s start with AWS.

In the June quarter, AWS posted $26.28 billion in sales, up 18.7 percent year on year and we think driven in large part by AI capacity but also due to enterprises spending less stingily on application modernization projects that involve moving to the cloud. There has been a server spending recession for general purpose compute since ChatGPT burst on the scene in late 2022, and we think there might have been a little one inside of the clouds as well during this time as companies tried to rebalance their budgets as GenAI went from an oddity to a necessity in the IT department.

Andy Jassy, who ran AWS for decades and who is now chief executive officer at Amazon, said as much on a call with Wall Street analysts going over the numbers for Q2:

“We’re continuing to see three macro trends drive AWS growth.”

“First, companies have completed the significant majority of their cost optimization efforts and are focused again on new efforts.

“Second, companies are spending their energy again on modernizing their infrastructure and moving from on-premises infrastructure to the cloud. This modernization enables builders to save money, innovate at a more rapid clip, and drive productivity in most companies’ scarcest resources, developers. This is the flip I’ve talked about in the past, where the vast majority of global IT spend today is on-premises, and we expect that to keep inverting over time. With the broadest functionality, the strongest security and operational performance, and the deepest partner ecosystem, AWS continues to be customers’ partner of choice and the biggest beneficiary of this flip from on-premises to the cloud.”

“And third, builders and companies of all sizes are excited about leveraging AI. Our AI business continues to grow dramatically with a multi-billion dollar revenue run rate despite it being such early days, but we can see in our results and conversations with customers that our unique approach and offerings are resonating with customers.”

Amazingly, AWS operating income rose by 74 percent to $9.33 billion, representing 35.5 percent of revenues, compared to a level of 24.2 percent in the year ago period. Renting out GPUs is a very lucrative business, as we showed for clouds in general this May and as we also showed for AWS in particular in July 2023. And that premium profit, thanks in large part to the scarcity of datacenter-class GPUs, is showing up in the AWS numbers.

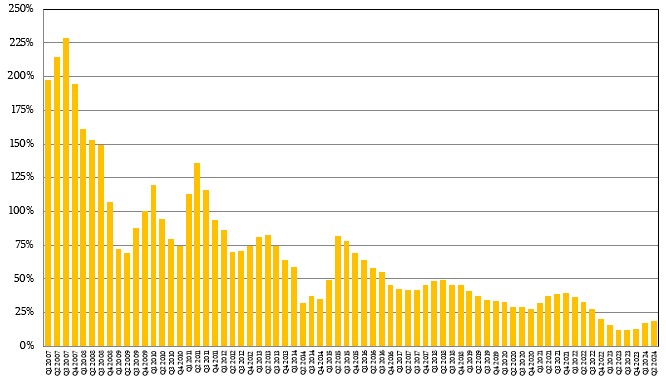

The demand for GPU accelerated systems is also driving overall growth for AWS, and has been doing so for the past several quarters, as you can see:

Long gone are the days when AWS was tripling and doubling every quarter, and so are the days when it was growing between 40 percent to 50 percent in late 2016 through early 2019. Even with the bump in cloud spending caused by the coronavirus pandemic starting in Q2 2020, the growth of AWS has never went above 40 percent and is averaging only 16 percent in 2023 and the first half of 2024.

The good news for Amazon is that AWS has been increasing its growth rate since bottoming out in the middle of 2023, and we think there is a good chance it could accelerate further for the remainder of 2024. But nothing crazy. Even the GenAI boom is not going to let AWS grow faster than 25 percent going forward, and mainly because it is only going to be able to get its hands on so many Nvidia and AMD GPUs and only be able to make so many of its own Trainium and Inferentia AI accelerators.

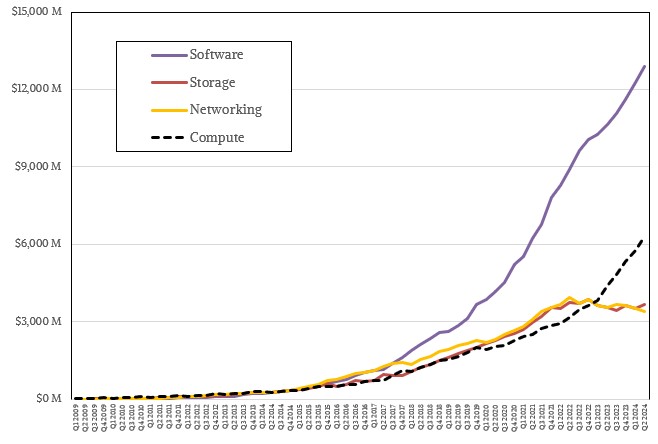

Looking at the growth rate of AWS is interesting, but we want to get a sense of how the AWS business breaks down across compute, storage, networking, and software. Amazon does not provide such a breakdown, but we have a model that does, and we will be the first to tell you that this model is not built on anything but a few strong hunches. AWS does not talk about its business this way, even though we think that it should.

Anyway, here is what the breakdown looks like according to our model:

Compute as a share of overall revenue for AWS bottomed out in late 2021 and early 2022, and that was with the early GPU instances that AWS sold for HPC and AI workloads in the mix pulling up the class average. Starting in 2022, the downward trend in spending on compute has, we think, reversed, and done so with a certain amount of vigor thanks to the high cost and high demand for AI servers.

Our model suggests that AWS sold $6.31 billion in compute in Q2 2024, up 42.4 percent, while storage was up 3.9 percent to $3.68 billion and networking was down 3.6 percent to $3.42 billion. Software, we think, represents just under half of AWS revenues, of $12.88 billion, in Q2 this year, and that is up 21.2 percent compared to the year ago period.

If you want to look at the “core” systems business at AWS, you add up compute, storage, and networking, and that comes to $13.4 billion in Q2. We think that this part of the business is drove maybe $4 billion in operating income, which works out to a little more than 30 percent of the revenue across those three systems pillars.

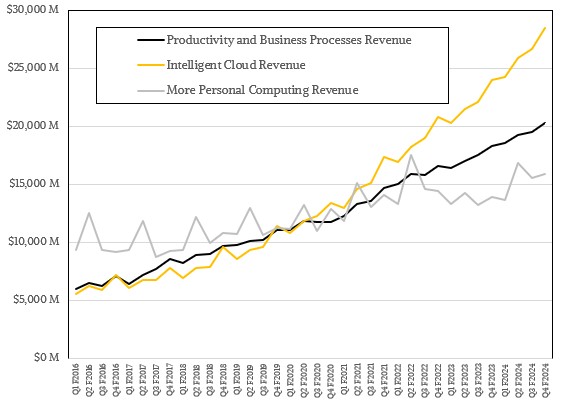

Now, let’s take a look at Microsoft’s cloud business, and its overall Azure and systems businesses. Starting with its three main groups:

The PC business and the application software businesses are great for Microsoft because they give fuel for the Azure cloud business, and indeed, many Microsoft customers run their PC and server applications in the cloud these days.

What we care about here at The Next Platform is the Intelligent Cloud group, which includes Windows Server, SQL Server, Visual Studio, and other middleware and tools sold into the datacenter, including compute, storage, and networking capacity on the Azure cloud and related platforms and SaaS services Microsoft peddles into the datacenter.

In Microsoft’s fourth quarter of fiscal 2024 ended in June, the Intelligent Cloud group had sales of $28.52 billion, up 18.8 percent, with operating income of $12.86 billion, up 22.2 percent. That operating income represents 45.1 percent of revenues, which is a tidy share indeed. (More profitable than the PC business, but less so than the application business, which stands to reason.)

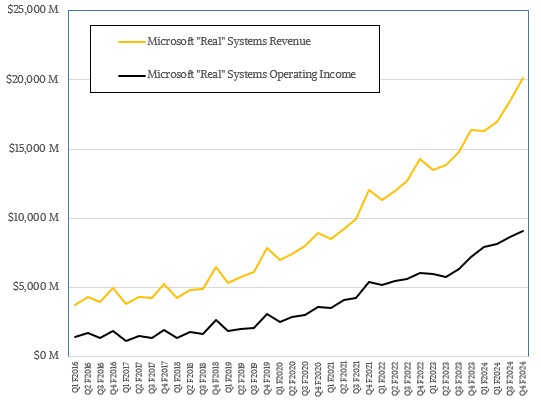

We have to do a whole lot of black spreadsheet magic to turn this figure for Intelligent Cloud into a useful number suitable for comparison with other clouds and other system makers. When we do that, we find that the “real” Microsoft systems business, comprising infrastructure and base system software on the Azure cloud and spread across tens of millions of datacenters worldwide, represented about $20.12 billion in sales in fiscal Q4, up 23 percent, and operating income was $9.07 billion, up 26.5 percent.

And if you strip away the on premises Windows Server stack software sold and rented during the quarter, then you can arrive at a revenue figure for the Azure cloud, which we think had $16.68 billion in sales, up 28.8 percent, and an operating income of $7.52 billion, up 32.3 percent year on year.

That leaves Google Cloud, which is the number three cloud player that definitely has to try harder and that has not yet found a way to be a profitable as AWS and Microsoft Azure as far as we can see.

In the second quarter, Google Cloud had $10.35 billion in revenues, up 28.8 percent, but it also posted an operating income of $1.17 billion, up by nearly 3X compared to the year ago quarter, So Google seems to be figuring this racket out a little. And perhaps by selling lots of TPU and GPU capacity for training AI models.

Now, let’s bring it all on home.

If you compare the system-level portions – meaning only compute, storage, and networking – of cloud revenues for the current quarters to their year ago quarters at AWS, Microsoft, and Google, there is an incremental $7.93 billion in revenue for the core systems businesses at these three clouds. How much of that came from the nearly $20 billion these companies invested in OpenAI and Anthropic? How much came from the unknown number of AI startups these companies might also have stakes in and who got such stakes only because the companies knew they had to spend most of that money on cloud capacity to train their models?

Inquiring minds want to know.

0 comments:

Post a Comment