Many of those claiming the markets could go up for a long while are now assuring investors a correction was overdue. So much for conventional wisdom.

The larger truth is that the era of easy money is ending just as price of recovery is coming at the cost of a debt burden - including yesterday's US budget deal - that may be unsustainable. Markets may overreact, they may well come roaring back, they may fall again, but just because you're paranoid, doesn't mean the reality isnt lying in plain sight. JL

Dambisa Moyo reports in Project Syndicate, Sarah Ponczek and colleagues report in Bloomberg:

The inevitable reckoning is beginning to dawn. The market is mispricing perennial structural challenges, in particular mounting and unsustainable global debt

and a dim fiscal outlook, particularly in the US, where the price of recovery is a growing deficit. In other words, short-term economic

gain is being supported by policies that threaten to sink the economy in

the longer term.

Project SyndicateAs 2018 progresses, business leaders and market participants should – and undoubtedly will – bear in mind that we are moving ever closer to the date when payment for today’s recovery will fall due. The capital market gyrations of recent days suggest that awareness of the inevitable reckoning is already beginning to dawn.

In recent days, the initial New Year optimism of many investors may have been jolted by fears of an economic slowdown resulting from interest-rate hikes. But no one should be surprised if the current sharp fall in equity prices is followed by a swift return to bullishness, at least in the short term. Despite the recent slide, the mood supporting stocks remains out of sync with the caution expressed by political leaders.

Market participants could easily be forgiven for their early-year euphoria. After a solid 2017, key macroeconomic data – on unemployment, inflation, and consumer and business sentiment – as well as GDP forecasts all indicated that strong growth would continue in 2018.

The result – in the United States and across most major economies – has been a rare moment of optimism in the context of the last decade. For starters, the macro data are positively synchronized and inflation remains tame. Moreover, the International Monetary Fund’s recent upward revision of global growth data came at precisely the point in the cycle when the economy should be showing signs of slowing.

Moreover, stock markets’ record highs are no longer relying so much on loose monetary policy for support. Bullishness is underpinned by evidence of a notable uptick in capital investment. In the US, gross domestic private investment rose 5.1% year on year in the fourth quarter of 2017 and is nearly 90% higher than at the trough of the Great Recession, in the third quarter of 2009.

This is emblematic of a deeper resurgence in corporate spending – as witnessed in durable goods orders. New orders for US manufactured durable goods beat expectations, climbing 2.9% month on month to December 2017 and 1.7% in November.

Other data tell a similar story. In 2017, the US Federal Reserve’s Industrial Production and Capacity Utilization index recorded its largest calendar year gain since 2010, increasing 3.6%. In addition, US President Donald Trump’s reiteration of his pledge to seek $1.5 trillion in spending on infrastructure and public capital programs will further bolster market sentiment.

All of this bullishness will continue to stand in stark contrast to warnings by many world leaders. In just the last few weeks, German Chancellor Angela Merkel cautioned that the current international order is under threat. French President Emmanuel Macron noted that globalization is in the midst of a major crisis, and Canadian Prime Minister Justin Trudeau has stated that the unrest we see around the world is palpable and “isn’t going away.”

Whether or not the current correction reflects their fears, the politicians ultimately could be proved right. For one thing, geopolitical risk remains considerable. Bridgewater Associates’ Developed World Populism index surged to its highest point since the 1930s in 2017, factoring in populist movements in the US, the United Kingdom, Spain, France and Italy. So long as populism lingers as a political threat, the risk of reactionary protectionist trade policies and higher capital controls will remain heightened, and this could derail economic growth.

Meanwhile the market is mispricing perennial structural challenges, in particular mounting and unsustainable global debt and a dim fiscal outlook, particularly in the US, where the price of this recovery is a growing deficit. In other words, short-term economic gain is being supported by policies that threaten to sink the economy in the longer term.

The Congressional Budget Office, for example, has forecast that the US deficit is on course to triple over the next 30 years, from 2.9% of GDP in 2017 to 9.8% in 2047, “The prospect of such large and growing debt,” the CBO cautioned, “poses substantial risks for the nation and presents policymakers with significant challenges.”

The schism in outlook between business and political leaders is largely rooted in different time horizons. For the most part, CEOs, hemmed in by the short termism of stock markets, are focused on the next 12 months, whereas politicians are focusing on a more medium-term outlook.

As 2018 progresses, business leaders and market participants should – and undoubtedly will – bear in mind that we are moving ever closer to the date when payment for today’s recovery will fall due. The capital market gyrations of recent days suggest that awareness of that inevitable reckoning is already beginning to dawn.

Bloomberg

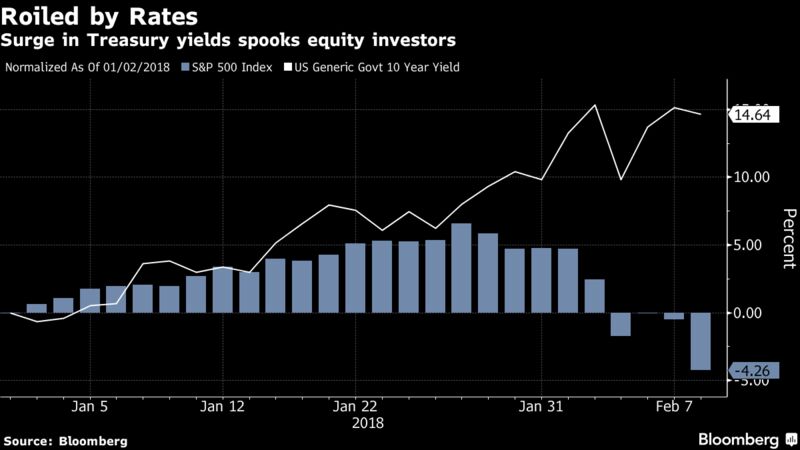

An era of low rates has ended and valuations are too high

The selling won’t stop from funds who were short volatility

Late Stage Expansion

Tiffany Wilding, executive vice president and economist, Pacific Investment Management Co.: “Absent a pickup in productivity growth, slowing payroll growth and rising economic capacity constraints should coincide with a gradual deceleration in real economic activity and building inflationary pressures. Along these lines, the weak labor productivity report released last week may raise questions about whether and to what extent productivity will rise over the coming year in response to fiscal expansion. Equity market behavior is mimicking historical periods of accelerating inflation, slowing growth.”

Correlated Pain

Eric Liu, head of research, Vanda Research:“The underlying drivers of risk aversion appear to have shifted once more. The ‘old fashioned’ risk-off environment that we witnessed at the start of the week -- with stocks and bonds moving in opposite directions -- seems to have subsided. Instead the market environment over the past 24 hours has mimicked last week’s pattern, with yields rising and stocks falling. Some things can’t be undone, however. Large shocks to the system tend to have a resetting effect, throwing hitherto rock-solid asset price correlations in disarray and reversing long-running trends.”

Flight to Safety

Peter Jankovskis, co-chief investment officer, Oakbrook Investments LLC: “There was definitely a flight-to safety component. If you look in terms of how various sectors performed, the sector that held up the best was utilities, followed by staples. The market worked its way to 2 percent and held there pretty well, and then all of a sudden in the last half hour or so took a bid dive at the end. There is a chance that might build for a base for a recovery tomorrow. Breaking the 10 percent correction, that may encourage people to try to put their

toes back in the market. We need to see what sort of follow through we have in Asia and Europe.”

Hedge Funds

Stephen Carl, head trader at Williams Capital Group: “Whatever trigger points hedge funds and money managers have, they are acting on it now. They can’t stand still. The session’s ending, the morning is going to be unknown, you have a potential shutdown on the brink as well, so that played out as well. But then, traders are bracing for Friday, the last day before a weekend. You saw a heavy selloff on Friday last week. The thinking is, if the market isn’t stable tomorrow there might be some additional selloff later in the day, like today.”

New Regime

Chad Morganlander, a portfolio manager at Washington Crossing Advisors, said by phone. “This is sell first, think about it later. The reality is, it’s been 10 years, and a lot of people that are in the market today have had ten years of a Federal Reserve that has artificially repressed volatility. And as they step away from that, reality starts to kick back in. There’s been a 10-year fantasy land that investors have been living in. And that’s a fairy tale that’s about to end.”

— With assistance by Kailey Leinz

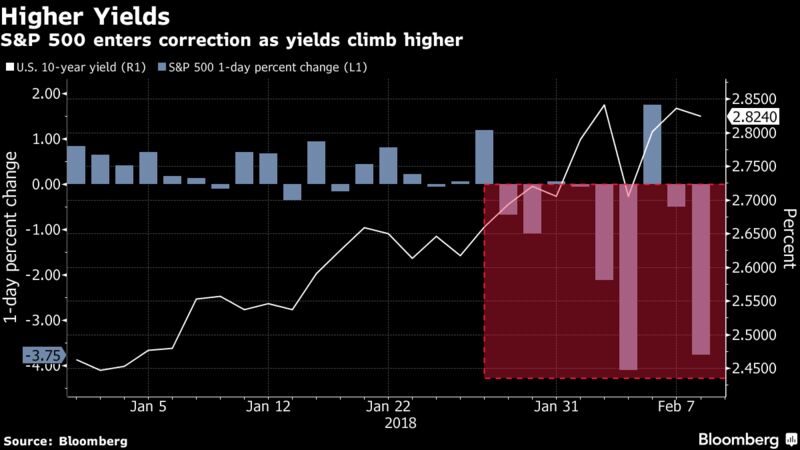

Stocks Plummet Into Correction as Rate Hike Jitters Return

Like everything in markets, this defies easy narratives. Is it rising yields, hedge funds selling out of arcane positions, inflated valuations bursting or none of the above? After two days of relative peace, investors theorized on what drove U.S. stocks into correction territory.

The Rate Wringer

Chris Rupkey, chief financial economist at MUFG Union Bank: “The era of low interest rates is at an end which means the proverbial punch in the punch bowl is leaving the party. And fast! The stock market is a leading economic indicator and right now it points the way for the economy straight down. There is no way the Federal Reserve is going to raise interest rates at Powell’s first meeting as chair in March. They aren’t that crazy.”

As a Partner and Co-Founder of Predictiv and PredictivAsia, Jon specializes in management performance and organizational effectiveness for both domestic and international clients. He is an editor and author whose works include Invisible Advantage: How Intangilbles are Driving Business Performance. Learn more...

The result – in the United States and across most major economies – has been a rare moment of optimism in the context of the last decade. For starters, the macro data are positively synchronized and inflation remains tame. Moreover, the International Monetary Fund’s recent upward revision of global growth data came at precisely the point in the cycle when the economy should be showing signs of slowing.Moreover, stock markets’ record highs are no longer relying so much on loose monetary policy for support. Bullishness is underpinned by evidence of a notable uptick in capital investment. In the US, gross domestic private investment rose 5.1% year on year in the fourth quarter of 2017 and is nearly 90% higher than at the trough of the Great Recession, in the third quarter of 2009.This is emblematic of a deeper resurgence in corporate spending – as witnessed in durable goods orders. New orders for US manufactured durable goods beat expectations, climbing 2.9% month on month to December 2017 and 1.7% in November.Other data tell a similar story. In 2017, the US Federal Reserve’s Industrial Production and Capacity Utilization index recorded its largest calendar year gain since 2010, increasing 3.6%. In addition, US President Donald Trump’s reiteration of his pledge to seek $1.5 trillion in spending on infrastructure and public capital programs will further bolster market sentiment.All of this bullishness will continue to stand in stark contrast to warnings by many world leaders. In just the last few weeks, German Chancellor Angela Merkel cautioned that the current international order is under threat. French President Emmanuel Macron noted that globalization is in the midst of a major crisis, and Canadian Prime Minister Justin Trudeau has stated that the unrest we see around the world is palpable and “isn’t going away.”Whether or not the current correction reflects their fears, the politicians ultimately could be proved right. For one thing, geopolitical risk remains considerable. Bridgewater Associates’ Developed World Populism index surged to its highest point since the 1930s in 2017, factoring in populist movements in the US, the United Kingdom, Spain, France and Italy. So long as populism lingers as a political threat, the risk of reactionary protectionist trade policies and higher capital controls will remain heightened, and this could derail economic growth.Meanwhile the market is mispricing perennial structural challenges, in particular mounting and unsustainable global debt and a dim fiscal outlook, particularly in the US, where the price of this recovery is a growing deficit. In other words, short-term economic gain is being supported by policies that threaten to sink the economy in the longer term.The Congressional Budget Office, for example, has forecast that the US deficit is on course to triple over the next 30 years, from 2.9% of GDP in 2017 to 9.8% in 2047, “The prospect of such large and growing debt,” the CBO cautioned, “poses substantial risks for the nation and presents policymakers with significant challenges.”The schism in outlook between business and political leaders is largely rooted in different time horizons. For the most part, CEOs, hemmed in by the short termism of stock markets, are focused on the next 12 months, whereas politicians are focusing on a more medium-term outlook.As 2018 progresses, business leaders and market participants should – and undoubtedly will – bear in mind that we are moving ever closer to the date when payment for today’s recovery will fall due. The capital market gyrations of recent days suggest that awareness of that inevitable reckoning is already beginning to dawn.

The result – in the United States and across most major economies – has been a rare moment of optimism in the context of the last decade. For starters, the macro data are positively synchronized and inflation remains tame. Moreover, the International Monetary Fund’s recent upward revision of global growth data came at precisely the point in the cycle when the economy should be showing signs of slowing.Moreover, stock markets’ record highs are no longer relying so much on loose monetary policy for support. Bullishness is underpinned by evidence of a notable uptick in capital investment. In the US, gross domestic private investment rose 5.1% year on year in the fourth quarter of 2017 and is nearly 90% higher than at the trough of the Great Recession, in the third quarter of 2009.This is emblematic of a deeper resurgence in corporate spending – as witnessed in durable goods orders. New orders for US manufactured durable goods beat expectations, climbing 2.9% month on month to December 2017 and 1.7% in November.Other data tell a similar story. In 2017, the US Federal Reserve’s Industrial Production and Capacity Utilization index recorded its largest calendar year gain since 2010, increasing 3.6%. In addition, US President Donald Trump’s reiteration of his pledge to seek $1.5 trillion in spending on infrastructure and public capital programs will further bolster market sentiment.All of this bullishness will continue to stand in stark contrast to warnings by many world leaders. In just the last few weeks, German Chancellor Angela Merkel cautioned that the current international order is under threat. French President Emmanuel Macron noted that globalization is in the midst of a major crisis, and Canadian Prime Minister Justin Trudeau has stated that the unrest we see around the world is palpable and “isn’t going away.”Whether or not the current correction reflects their fears, the politicians ultimately could be proved right. For one thing, geopolitical risk remains considerable. Bridgewater Associates’ Developed World Populism index surged to its highest point since the 1930s in 2017, factoring in populist movements in the US, the United Kingdom, Spain, France and Italy. So long as populism lingers as a political threat, the risk of reactionary protectionist trade policies and higher capital controls will remain heightened, and this could derail economic growth.Meanwhile the market is mispricing perennial structural challenges, in particular mounting and unsustainable global debt and a dim fiscal outlook, particularly in the US, where the price of this recovery is a growing deficit. In other words, short-term economic gain is being supported by policies that threaten to sink the economy in the longer term.The Congressional Budget Office, for example, has forecast that the US deficit is on course to triple over the next 30 years, from 2.9% of GDP in 2017 to 9.8% in 2047, “The prospect of such large and growing debt,” the CBO cautioned, “poses substantial risks for the nation and presents policymakers with significant challenges.”The schism in outlook between business and political leaders is largely rooted in different time horizons. For the most part, CEOs, hemmed in by the short termism of stock markets, are focused on the next 12 months, whereas politicians are focusing on a more medium-term outlook.As 2018 progresses, business leaders and market participants should – and undoubtedly will – bear in mind that we are moving ever closer to the date when payment for today’s recovery will fall due. The capital market gyrations of recent days suggest that awareness of that inevitable reckoning is already beginning to dawn.

0 comments:

Post a Comment