The result will likely be an eventual decline in valuations as the equity markets' terrible year shows no end thanks, in part, to the US Federal Reserve's push to raise interest rates in order to tamp down inflation. JL

Marc Vartabedian reports in the Wall Street Journal:

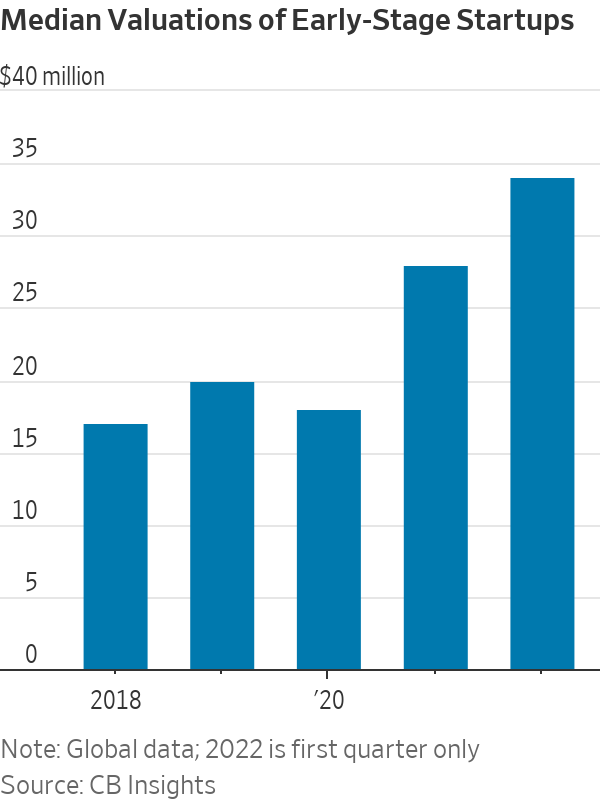

Investors committed $144 billion to startups globally in the first quarter, down 19% from the prior quarter, the largest percentage decline since the third quarter of 2012. The number of deals completed also dropped, falling 5%. At the same time, valuations continued to rise, causing some investors to expect a price drop for startups this year. Investors attributed the continued increase in valuations in part to the so-called dry powder- capital raised that has yet to be invested. The median valuation of early-stage startups last quarter rose 21%. The median valuation of midstage startups rose 15%. Some investors predict valuations will fall as the public-market pullback trickles down to the private market.After setting a feverish investing pace last year, venture capitalists took their foot off the gas in this year’s first quarter. At the same time, valuations largely continued to rise, a dynamic that is causing some investors to expect a price drop for startups this year.

Investors committed $144 billion to startups globally in the first quarter, down 19% from the prior quarter, which is the largest percentage decline since the third quarter of 2012, according to analytics firm CB Insights. The number of deals completed also dropped, falling 5% compared with the fourth quarter to 8,835.

Meanwhile, valuations, a measure of the price investors pay for stakes in startups, continued on what has been a significant increase in recent years as investors plow capital into fledgling technology companies.

The median valuation of early-stage startups last quarter rose 21% to $34 million compared to all of last year, according to CB Insights. The median valuation of midstage startups rose 15% to $343 million for the same periods.

“There was a lot more investor energy chasing us in the fourth quarter than in the first quarter,” said Anshu Prasad, the co-founder and chief executive of transportation logistics startup Leaf Logistics Inc. Mr. Prasad said he started fundraising last summer.

Still, he said that negotiations with investors around his startup’s valuation were hardly a sticking point when the company closed a $37 million Series B deal in January. The financing valued Leaf at $262 million, a 274% jump from the valuation the company received in 2019 when it last raised capital.

Investors said rising inflation and interest rates as well as the public-market downturn put pressure on the venture market. Rising interest rates have historically led investors to shift capital away from venture toward bonds as their yields increase, giving investors higher payouts.

Investors attributed the continued increase in valuations in part to the mountain of so-called dry powder—capital raised that has yet to be invested—that venture firms have at their disposal.

“There has been so much capital raised in the last 24 months in the early stages and very large early-stage funds across the board that the supply-and-demand balance between deals and capital still supports rising valuations, for now,” said Zach DeWitt, a partner at venture firm Wing VC.

This dynamic comes as other areas of the venture market have sputtered. Initial public offerings, one of the primary ways venture investors get paid out for their investments, have nearly ground to a halt.

To be sure, even with the drop in funding during the first quarter, the period still netted the fourth-largest funding haul on record and was 7% more than the same quarter in 2021.

Some investors predict valuations will fall as the public-market pullback trickles down into the private market. There is often a lag in the public market’s effect on private-company dealmaking.

Already, late-stage startups, which are closest to the public market as they near initial public offerings, experienced a dip in median valuations, falling 4% to $1.05 billion, according to CB Insights. So-called mega-round financings of at least $100 million, which typically occur at later stages of investing, experienced a 30% drop in the first quarter to $74 billion compared with the prior quarter.

“I think [dropping valuations] will hit midstage next. It’s the next most logical area to get hit,” Sozo Ventures Managing Director Spencer Foust said.

While lower valuations are often associated with market slowdowns, venture investors often welcome such drops as opportunities to invest in companies on more favorable terms. That also can temper startups’ expectations and make follow-on rounds easier to close.

Startup valuations have been on a tear in recent years, driven in part by nontraditional venture investors, such as hedge funds and corporations, entering the asset class. Median late-stage valuations, for instance, have soared 653% since 2018, according to CB Insights.

Lux Capital Partner Bilal Zuberi says he expects startup prices to drop this year as more investors begin to see their portfolio companies experience valuation markdowns.

“It psychologically pushes funds to reassess their entry prices,” Mr. Zuberi said.

History points to a correction in private-company valuations, said Ginger Chambless, a managing director and head of research for JPMorgan Chase Commercial Banking, in a Q&A as part of a report by analytics firm PitchBook Data Inc. and the National Venture Capital Association.

“Historically, there has been a one- to two-quarter lag between a public markets correction and the private markets,” Ms. Chambless said.

0 comments:

Post a Comment