Research: The Reason Firm Age Is a Main Determinant of Growth

Just as people - and artificial intelligence - get smarter as they learn more, so do organizations. The result is that they tend to both drive growth and benefit from it.

This research is especially interesting in light of popular perceptions about tech disruption of the economy. The implication may bethat those enterprises able to adapt tend to grow and survive - as in, all companies are now tech companies - whereas those that cannot do so fail. JL

Marko Melolinna and Patrick Schneider report in Bank Underground:

Firms’ lifecycles – being born, aging and dying – are linked to how

firms grow. The results show that, as they age, firms grow mainly by employing more people, rather than by generating

more turnover per employee. And while firms are on average less likely

to die the older they get, the cohort of firms that were born since the

financial crisis are more resilient than older firms.There is a selection effect of surviving firms driving growth, as

well as a reallocation effect towards the more productive firms. Firm age is a main determinant of firm growth and survival. For example, older firms are likely to be larger and grow more slowly than younger ones (see Audretsch & Mata, 1995; Coad et al, 2013). They are also more likely to survive (see Audretsch & Mahmood, 1995, Manjón-Antolín & Arauzo-Carod, 2008). This is why, in this blog post, we look at how firms’ lifecycles – firms being born, aging and dying – are linked to how firms grow. The results show that, as they age, firms in the United Kingdom grow mainly by employing more people, rather than by generating more turnover per employee. And while firms are on average less likely to die the older they get, the cohort of firms that were born since the financial crisis are more resilient than older firms.

To conduct the analysis, we need firm-level data on UK firms over time, including information on when a particular firm was born and when it died. We use the ONS’s Business Structure Database (BSD), which provides key information, like turnover, the number of employees and the number of locations of all active enterprises in the UK in April each year over 1997-2017. On average, there are over 2 million enterprises annually in the BSD. For this analysis, we take the dataset as given with two exceptions – we drop finance sector firms, and we drop the first and last years of the data. This is due to the large number of outliers and breaks in aggregate figures in these dimensions of the BSD.

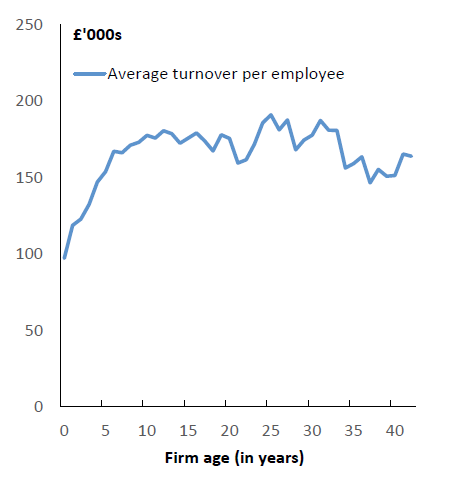

We look at the data in a few different ways. First, dividing the aggregate turnover by the employment variable for each firm gives us a measure of turnover productivity. This definition of productivity is slightly different from how it is typically defined when looking at aggregate data, which uses value added per employee. But the definitions are sufficiently close for the analysis here to be meaningful. Looking at the turnover productivity variable unconditionally (in other words, without controlling for firm- or time-specific effects) by age suggests that firms get more productive as they mature, up to around 10 years of age. After that, the average level of productivity is flat, and even slightly lower in the older firms (Chart 1). From the data, we also know that the average age of UK firms has increased over time. Hence, based on these unconditional averages, the higher average age doesn’t necessarily explain the fact that aggregate productivity has grown. Chart 1: Unconditional productivity by age of firm

The chart shows turnover per employee in 2015 GBP.

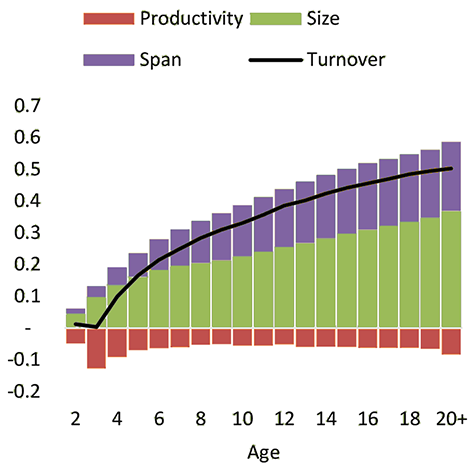

Second, to study the lifecycle effects on growth more precisely, we can split the turnover variable for each firm in the sample into three margins; productivity (turnover divided by the number of employees), size (the number of employees divided by the number of locations from which the firms operates) and span (the number of locations for each firm). By taking logarithms of the three margin variables, they sum up to the logarithm of turnover. We can then study the contribution of the margins on turnover growth in a regression framework, also taking into account lifecycle effects. Chart 2 shows the results of such a regression, which also controls for firm- and time-specific effects, and uses the whole BSD sample. Turnover is increasing with age. This growth over the lifecycle is, on average, driven by persistent increases in size as firms age, and by a moderate span effect that seems to come through in the first ten years of a firm’s life. Productivity does not drive turnover growth, on average, over the lifecycle. In other words, age alone does not make firms more productive. But we know from the data that over time the average age of firms has increased and that the economy as a whole still tends to get more productive over time. One possible way to explain this is that there is a selection effect; firms are more likely to survive if they are productive as well as resources being reallocated towards these more productive firms. Chart 2: Contributions to cumulative log-turnover growth by age of firm

The chart shows the marginal effect of aging for each margin as a contribution to (logarithm of) turnover.

We can also examine lifecycle dynamics in terms of cohorts, in other words, separating enterprises by birth year. We focus here on two cohorts – enterprises born before the financial crisis in 2008 (‘pre-crisis’), and the rest ‘post-crisis’ – to see what effect the financial crisis had on the path to maturity and survival of firms.

The results of the analysis suggest that firms born since the crisis have, on average, grown through employment by more than those born before, and they have increased their size by more with a smaller span. However, there is no clear evidence of large differences in productivity between the two cohorts as firms age. Hence, there is no evidence that firms born since the crisis have a more negative effect on UK productivity growth than older firms.

The post-crisis cohort also has better survival chances beyond the age of two. Chart 3 shows the estimated survival probabilities for firms from the two cohorts (pre- and post-crisis). While the probability of death generally declines with age, there is a statistically significant lower probability of death among firms born since the crisis for any age except very soon after birth. One potential explanation for this phenomenon is a selection effect at birth. The post-crisis cohort came into existence in the harshest economic conditions in a generation (see, for example, ONS (2018)). We would expect these harsh conditions to discourage the entry of weaker firms (see Melitz, 2003). With our analysis, we cannot prove or disprove this hypothesis. But the results are consistent with it and whatever the reason, post-crisis cohorts appear to be more resilient than those born before the crisis. Chart 3: Cohort likelihood of death by age

The chart shows the probability of firm death, based on a hazard function probit estimator.

To conclude, even though the population of UK firms has got older over time, firms do not appear to get more productive just by aging. Firms born since the financial crisis are no less productive than the ones born before it and hence, they do not explain weak productivity growth in the UK in the past decade. Furthermore, survival likelihood of UK firms increases as they age. Over time, it is possible that there is a selection effect of the surviving firms driving growth, as well as a reallocation effect towards the more productive firms.

This work was produced using statistical data from ONS. The use of the ONS statistical data in this work does not imply the endorsement of the ONS in relation to the interpretation or analysis of the statistical data. This work uses research datasets which may not exactly reproduce National Statistics aggregates.

You can download many paid applications to no end on your contraption and put aside additional money, any application you need. Most by far of the renowned paid applications are available on appvn . To value this segment, you don't need to pay by any stretch of the creative ability. Other than that, it in like manner offers endless download. It infers you can download any application you need whatever number as could be permitted.

As a Partner and Co-Founder of Predictiv and PredictivAsia, Jon specializes in management performance and organizational effectiveness for both domestic and international clients. He is an editor and author whose works include Invisible Advantage: How Intangilbles are Driving Business Performance. Learn more...

1 comments:

You can download many paid applications to no end on your contraption and put aside additional money, any application you need. Most by far of the renowned paid applications are available on appvn . To value this segment, you don't need to pay by any stretch of the creative ability. Other than that, it in like manner offers endless download. It infers you can download any application you need whatever number as could be permitted.

Post a Comment