People could be forgiven for thinking the evolution of the tangible - like steel mills - to the intangible - like software - was the endgame of the tech revolution.

After all, how much more dramatic does this need to be? Hard assets becoming fungible pawns in a global game of value migration while all that soft stuff that serious people once assigned to sons-in-law lacking advanced skills suddenly erupted in ways that resulted in young dudes leading enterprises whose names you have trouble pronouncing making more money than hedge fund managers.

But, as the following article explains, this is just the beginning. Phase Two of whatever revolution we now think we are in is going to mandate the disappearance of all those little devices to which the industry has assured we are now hopelessly addicted. Because if technology has taught us anything, it is that middlemen are inefficient and, arguably, rather less convenient than the direct current of consumer to vendor interaction.

Siri and Echo may have seemed like cutesy appendages to the more serious business of selling stuff you can weigh and count. While you weren't looking, though, they are becoming the forces that tell you how, when and where to do so. Adapt or evaporate. JL

Chris Dixon reports in Medium:

The next big step will be for the “device” to fade

away. The computer — whatever its form will

be an intelligent assistant. We will move

from mobile first to an AI first world — which in most cases will mean voice interfaces — (as they)

become the master routers of the internet economic loop, rendering many

of the other layers interchangeable or irrelevant. Voice is a

novelty today, but in technology the next big thing often starts out looking that way.

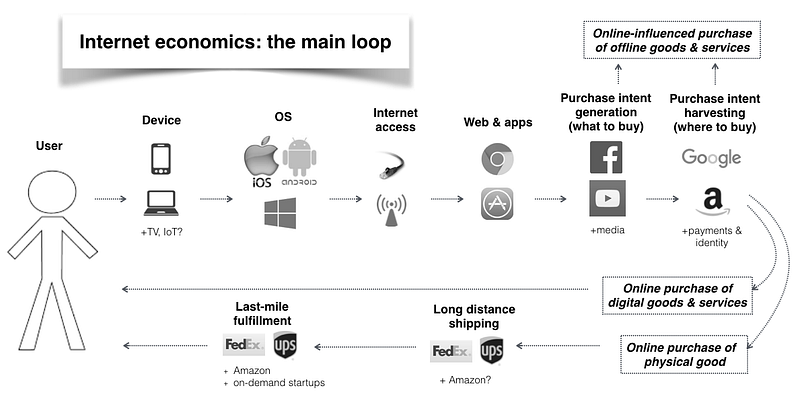

We are living in an era of bundling. The big five consumer tech companies — Google, Apple, Facebook, Amazon, and Microsoft — have moved far beyond their original product lines into all sorts of hardware, software, and services that overlap and compete with one another. But their revenues and profits still depend heavily on external technologies that are outside of their control. One way to visualize these external dependencies is to consider the path of a typical internet session, from the user to some revenue-generating action, and then (in some cases) back again to the user:

When evaluating an internet company’s strategic position (the defensibility of its profit moat), you need to consider: 1) how the company generates revenue and profits, 2) the loop in its entirety, not just the layers in which the company has products.

For example, it might seem counterintuitive that Amazon is a major threat to Google’s core search business. But you can see this by following the money through the loop: a significant portion of Google’s revenue comes from search queries for things that can be bought on Amazon, and the buying experience on Amazon (from initial purchasing intent to consumption/unboxing) is significantly better than the buying experience on most non-Amazon e-commerce sites you find via Google searches. After a while, shoppers learn to skip Google and go straight to Amazon.

Think of the internet economic loop as a model train track. Positions in front of you can redirect traffic around you. Positions after you can build new tracks that bypass you. New technologies come along (which often look toy-like and unthreatening at first) that create entirely new tracks that render the previous tracks obsolete.

There are interesting developments happening at each layer of the loop (and there are many smaller, offshoot loops not depicted in the chart above), but at any given time certain layers are industry flash points. The most prominent recent battle was between mobile devices and operating systems. That battle seems to be over, with Android software and iOS devices having won. Possible future flash points include:

The automation of logistics. Today’s logistics network is a patchwork of ships, planes, trucks, warehouses, and people. Tomorrow’s network will include significantly more automation, from robotic warehouses to autonomous cars, trucks, drones, and delivery bots. This transition will happen in stages, depending on the economics of specific goods and customers, along with geographic and regulatory factors. Amazon of course has a huge advantage in logistics. Google has tried repeatedly to get into logistics with little success. On-demand ride-sharing and delivery startups could play an interesting role here. The logistics layer is critical for e-commerce, which in turn is critical for monetizing search. Amazon’s dominance in logistics gives it a very strong strategic moat as e-commerce continues to take market share from traditional retail.

Web vs apps. The mobile web isarguably in decline: users are spending more time on mobile devices, and more time in apps instead of web browsers. Apple has joined the app side of this battle (e.g. allowing ad blockers in Safari, encouraging app install smart banners above websites). Facebook has also taken the app side (e.g. encouraging publishers to use Instant Articles instead of web views). Google of course needs a vibrant web for its search engine to remain useful, so has joined the web side of the battle (e.g. punishing websites that have interstitial app ads, developing technologies that reduce website loading times). The realistic danger isn’t that the web disappears, but that it gets marginalized, and that the bulk of monetizable internet activities happen in apps or other interfaces like voice or messaging bots. This shift could have a significant effect on web publishers who rely on older business models like non-native ads, and could make it harder for small startups to grow beyond niche use cases.

Video: from TV to mobile devices. Internet companies are betting that video consumption will continue to shift from TV to mobile devices.The hope is that this will not only create compelling user experiences, but also unlock access to the tens of billions of ad dollars that are currently spent on TV.

“I think video is a mega trend, almost as big as mobile.” — Mark Zuckerberg

Last decade, the internet won the market for ads that harvest purchasing intent (ads that used to appear in newspapers and yellow pages), with most of the winnings going to Google. The question for the next decade is who will win the market for ads that generate purchasing intent (so far the winner is Facebook, followed by Google). Most likely this will depend on who controls the user flow to video advertising. Today, the biggest video platforms are Facebook and YouTube, but expect video to get embedded into almost every internet service, similar to how the internet transitioned from text-heavy to image-heavy services last decade.

Voice: baking search into the OS. Voice bots like Siri, Google Now, and Alexa embed search-like capabilities directly into the operating system. Today, the quality of voice interfaces isn’t good enough to replace visual computing interfaces for most activities. However, artificial intelligence is improving rapidly. Voice bots should be be able to handle much more nuanced and interactive conversations in the near future.

Amazon’s vision here is the most ambitious: to embed voice services in every possible device, thereby reducing the importance of the device, OS, and application layers (it’s no coincidence that those are also the layers in which Amazon is the weakest). But all the big tech companies are investing heavily in voice and AI. As Google CEO Sundar Pichai recently said:

The next big step will be for the very concept of the “device” to fade away. Over time, the computer itself — whatever its form factor — will be an intelligent assistant helping you through your day. We will move from mobile first to an AI first world.

This would mean that AI interfaces — which in most cases will mean voice interfaces — could become the master routers of the internet economic loop, rendering many of the other layers interchangeable or irrelevant. Voice is mostly a novelty today, but in technology the next big thing often starts out looking that way.

As a Partner and Co-Founder of Predictiv and PredictivAsia, Jon specializes in management performance and organizational effectiveness for both domestic and international clients. He is an editor and author whose works include Invisible Advantage: How Intangilbles are Driving Business Performance. Learn more...

0 comments:

Post a Comment