The World's Inevitable Cognitive Decline - and Its Positive Implications

No, the US is not necessarily facing moral, political, military or economic decline. At least not according to the data. But it's population is aging, which means the brains of all those Boomers, already addled by their earlier experimentation may start to decline functionally at a faster rate.

This is neither good nor bad, just a function of the so-far inevitable aging process. The question is how businesses will respond since many of those cognitively challenged will still be the consumers withe the greatest disposable income. And therein lies the opportunity for tech designers and engineers. JL

Justin Fox reports in Bloomberg:

Cognitive function really starts to go downhill for people in their 70s.

The eldest of the baby boomers will start turning 70

in January Adult life is one long, sad tale of declining analytic capability and ability to remember things. I could tell you all about my personal experience with this, except that of course I've forgotten most of it.

There is an accompanying long, happy tale, though, of increasing wisdom and skill. When you put the two together, you get this:

source: david laibson

This is from a slide deck by Harvard economics professor David Laibson. The estimate that cognitive function peaks at age 53 comes from a 2009 paper by Laibson, Sumit Agarwal, John C. Driscoll and Xavier Gabaix titled "The Age of Reason: Financial Decisions over the Life Cycle and Implications for Regulation." The four economists examined the fees and interest rates paid by thousands of borrowers in 10 different types of credit transactions, and found that, on average, such costs were minimized at age 53.3.

I've known about this paper for a while, read and reread it as I've gotten closer to 53, and referred to it in columns. But this week I saw Laibson present the findings at a conference, and two things stood out. One is that cognitive function really starts to go downhill for people in their 70s. The other is that the eldest of the baby boomers will start turning 70 in January.

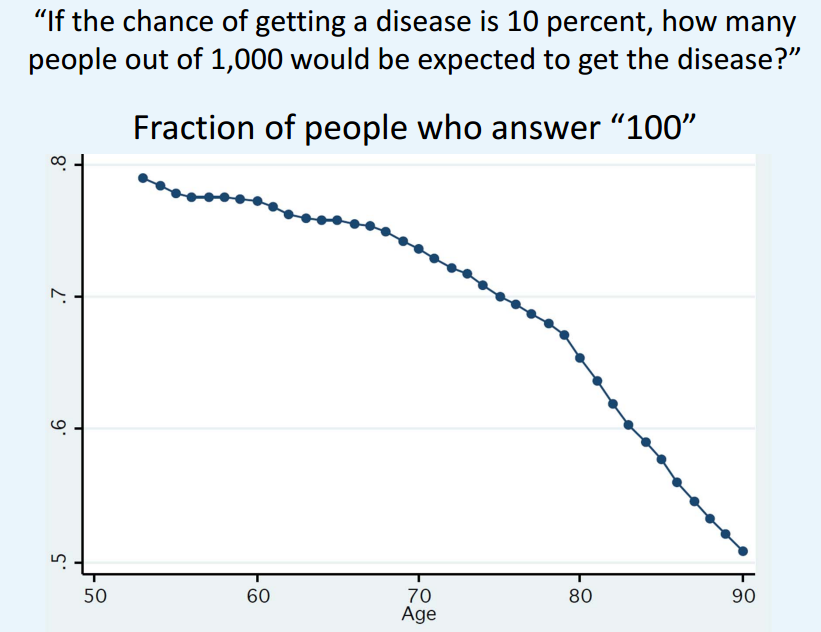

Here, for example, is another chart from Laibson's slideshow, using longitudinal data from the University of Michigan's Health and Retirement Study:

The percentage of wrong answers accelerates in subjects' late 60s, and again around age 80. Other measures show different inflection points, but the general message is that cognitive decline is relatively slow in people's 50s and 60s, then really gets going around age 70.

These are just averages, of course, and I'd like to state right here that every over-70 person I happen to be related to or work with is way out there on the high-cognitive-function edge of the dispersion. But as the members of the giant baby-boom generation move into their 70s, and their elders live longer and longer, it seems inevitable that the ranks of Americans who don't know that 10 percent of 1,000 is 100 are going to grow in the coming years. To put it another way, data cited in the Agarwal, Driscoll, Gabaix and Laibson paper indicate that "about half the population aged 80–89 have a diagnosis of either dementia or cognitive impairment without dementia." That population is already growing, and the numbers will really explode when the baby boomers start hitting 80 a decade from now.

Laibson, who has done a lot of research over the years on retirement savings, is most concerned about the impact in that age group. Perversely, government policy in the U.S. has long protected savers in their 40s and 50s while generally leaving those in their 70s and 80s to the wolves. That is, the 401(k) plans in which people stow most retirement savings while they're still working are governed by the Employee Retirement Income Security Act, which requires plan sponsors (employers, mostly) to act as fiduciaries who have to look out for the best interests of plan members. The Individual Retirement Accounts into which people often roll over those 401(k) balances when they retire are not.

This is useful context for understanding the Obama administration's big push to require brokers to act as fiduciaries when advising clients on their retirement savings. It's much harder to argue that brokerage clients are grown-ups who should be able to look out for themselves when you consider that the most important clients for brokers peddling retirement products are people over the age of 65 who are facing a rapid decline in their ability to make smart financial decisions.

This rapid decline, and the aging of the baby boomers, also makes me wonder about the political system in the U.S. (and other aging nations) over the next few decades. If you don't like the decisions voters make now, think of what it will be like as the percentage of voters with cognitive impairments grows. The share of impaired elected officials may grow, too. After all, Donald Trump will turn 70 next year. Hillary Clinton will get there in 2017.

Then again, Ronald Reagan turned 70 a week after taking office in 1981, and he's generally seen as having been quite an effective president. There are signs that he was suffering from cognitive decline in his second term, but he had an infrastructure around him to aid in decision-making. Also -- and this is important -- he didn't have to drive anywhere.

The evidence on driving is similar to that on answering questions about percentages -- people start to get significantly worse at it in their late 60s, and per-mile fatalities really spike around age 80. I have reason to hope, though, that advances in self-driving vehicles will bail me out and that, like Ronald Reagan, I won't have to drive after I'm 70.

New technologies could compensate for cognitive decline in other ways, too, just as Reagan's aides surely did for him. I already rely on Google and Evernote to remember things for me, and I carry around a calculator app on my smartphone that can help me if I'm having trouble with my percentages. There are those who argue that these tools make us dumber, and they may be right, but for those on the decline side of the cognitive function curve the effect has to be mostly positive. I'm not exactly thrilled at the prospect of the singularity, but if machines can make us all smarter and safer in our declining years, that's a pretty big upside.

As a Partner and Co-Founder of Predictiv and PredictivAsia, Jon specializes in management performance and organizational effectiveness for both domestic and international clients. He is an editor and author whose works include Invisible Advantage: How Intangilbles are Driving Business Performance. Learn more...

0 comments:

Post a Comment