Tech Productivity, Capital Markets and the Rest of the Global Economy

Capital markets cratered last week which, as usual, spurred a hunt for culprits. China is an obvious one: much of the developed world has been putting bread on the table by selling the Chinese whatever they want, which has been pretty much everything anyone could think of. But as optimists whose beliefs are confirmed are wont to do, China rode that trend a little too long and way too hard, leading to the types of ridiculous overinvestment that cause economiesto choke on their own excess.

But the other cause may be that western faith in the abiding ability of technology to solve every economic and social problem. There is now a debate, as the following article explains, about whether the major productivity gains have already been booked and the current spate of restaurant-finding or dating apps is just fluff.

It is not surprising that the financiers are claiming the problem is government data gathering, not tech: they have gotten rich off of tech and don't want the party to end. The reality may be that we are now in a period of tech digestion and adaptation which will produce benefits in the future. The issue is that reaching that verdant, misty upland may just take a while. JL

Noah Smith comments in Bloomberg:

From the early 1970s through the early 1990s, when productivity slowed

dramatically, only to zoom ahead in the late '90s and early 2000s. Now

the numbers are slowing again. One of the key debates about economics is whether new technology is making us more productive. This is very important, since productivity has been the key to the vast increases in human living standards in developed countries during the past two centuries. There was a scare from the early 1970s through the early 1990s, when productivity slowed dramatically, only to zoom ahead in the late '90s and early 2000s. Now the numbers are slowing again, and economists are worried. How does the tech industry fit into all this as the economy returns to something resembling normality? In terms of productivity, is tech our salvation, or a false hope?

On one side of the debate, we have John Fernald of the Federal Reserve Bank of San Francisco, an expert on measuring technological productivity. On the other side, we have the economics research team of Goldman Sachs, one of the most respected in the private sector. The quality of our future could hinge on which one of these heavyweights is right.

Traditionally, when economists wanted to figure out how productive technology makes our economy, they just netted out the contributions of "factors of production" such as labor and capital, and whatever is left over -- called total factor productivity -- was regarded as technology's contribution. Fernald realized that this was an oversimplification, since it didn't take into account other factors -- like how intensively capital was used. He carefully "purified" the measurement of technological productivity, and came up with numbers that were very different from what economists were using. Now, Fernald's numbers are considered the gold standard.

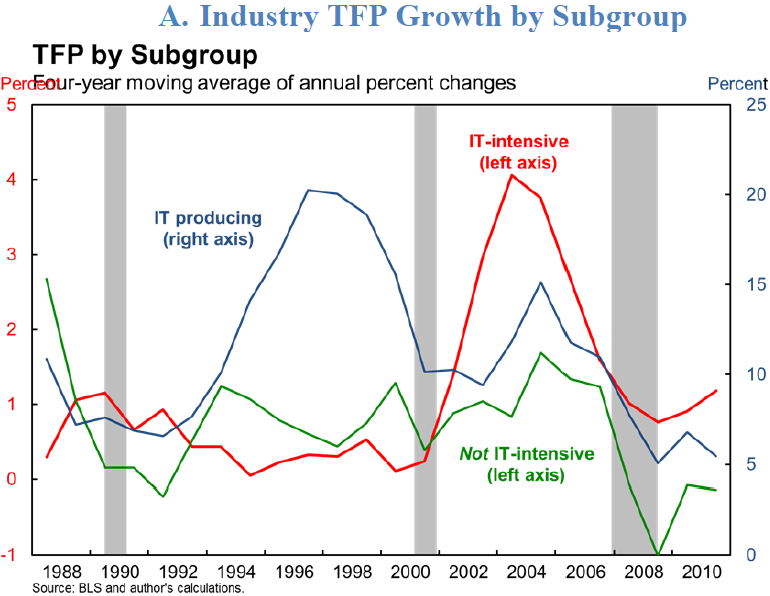

In 2014, Fernald wrote a paper titled "Productivity and Potential Output Before, During, and After the Great Recession." The paper confirms that since about 2003 -- well before the Great Recession -- measured productivity growth had slowed down. But Fernald also looked specifically at industries that either produce information and communication technologies , or use these technologies intensively -- in other words, IT industries.

What Fernald found was that IT industries contributed a lot to the productivity boom in the late '90s and early '00s. But then IT-related productivity slowed dramatically. Here is a graph from Fernald's paper: The blue line is productivity growth for companies that make IT. It boomed spectacularly in the '90s, experienced a smaller boom in the '00s, and then fell to a more modest rate of growth. Though these industries are still getting more productive at a steady clip, it's no longer fast enough to power rapid productivity growth in the wider economy.

The red line represents companies that use a lot of IT but don't produce it themselves. These companies experienced a productivity boom in the '00s, but those gains have mostly petered out. As for other companies -- the green line on the graph -- their productivity is now crawling along.

Fernald's data is very worrying -- if he's right, it suggests that the IT boom was a short hiccup in a long-term slowdown.

But economists Jan Hatzius and Kris Dawsey of Goldman Sachs are skeptical of Fernald's finding. They note that the stock prices of tech companies are high, meaning that investors expect big things in the sector. Profit margins -- not a measure of productivity, to be sure, but an indicator of companies' overall health -- have also risen.

What could be going on? Is the market overvaluing tech companies, or are they more productive than Fernald's numbers suggest? Hatzius and Dawsey suspect that national economic statistics themselves are to blame. They note that it's very difficult to measure the quality of IT products. If quality increases while prices and sales stay the same, productivity has gone up, but official statistics won't record the increase. There is also the problem that innovation in IT regularly produces new kinds of products, which people use to replace old kinds of products. When this happens, the overall cost of living goes down -- for example, if people read free social media instead of watching TV for their entertainment. But economists measure inflation by measuring changes in prices for the same goods, so they will miss this kind of change, and end up overstating inflation -- which understates productivity.

A burst of innovation could therefore be causing official IT productivity growth numbers to plummet, even as it increases true productivity by improving quality and introducing new goods. If the official statistics are biased, then even the meticulous, brilliant Fernald won't be able to get meaningful results from the data.

So this is the debate. If you believe that the official price statistics give an accurate measure of the cost of IT, then you should be worried about a slowdown in the sectors. But if you think that the unique nature of IT makes price statistics unreliable, then you shouldn't be worried.

As a Partner and Co-Founder of Predictiv and PredictivAsia, Jon specializes in management performance and organizational effectiveness for both domestic and international clients. He is an editor and author whose works include Invisible Advantage: How Intangilbles are Driving Business Performance. Learn more...

0 comments:

Post a Comment